In the rapidly evolving world of fintech, two heavyweights, Apple and PayPal, have long vied to dominate digital payments and innovative financial services. Both companies ventured into the “buy now, pay later” (BNPL) sector—PayPal launched its Pay Later feature in 2021, and Apple followed with Apple Pay Later in October 2023 (albeit only in the United States at first). While both services share common ground, recent developments—including Apple’s decision to discontinue Apple Pay Later—reveal much about the broader market, user preferences, and the rapidly shifting competitive landscape.

In this article, we delve into the details behind Apple Pay Later and PayPal Pay Later, how each service aimed to capture market share, and how market reactions and leadership decisions have shaped their futures.

1. A Quick Overview of BNPL Services

BNPL, or “buy now, pay later,” allows users to receive goods immediately and defer payment across smaller installments—often without extra interest or fees, provided they abide by specific repayment timelines. This appeal has made BNPL services a convenient alternative to traditional credit cards and layaway plans. Many e-commerce platforms and digital payment providers have quickly adopted BNPL features, and consumer demand has soared, especially during periods of economic uncertainty.

2. PayPal Pay Later at a Glance

Launch and Global Reach

-

Initial Launch: PayPal introduced its Pay Later service in 2021, focusing first on the United States. It quickly gained traction by integrating seamlessly into PayPal’s existing checkout experiences.

-

International Variations: Policies differ by country, with various maximum amounts, installment numbers, and interest-free options:

-

United States & Australia: Users can split purchases from $30 up to $1,500 into four interest-free installments.

-

France: Four interest-free installments for amounts between €30.00 and €2,000.

-

United Kingdom: Three interest-free installments on purchases from £30.00 to £2,000.

-

How It Works

-

Select “Pay Later” Option: When ready to check out, users can opt for PayPal Pay Later if their transaction meets the necessary requirements (amount, location, and user account standing).

-

System Assessment: PayPal evaluates the user’s eligibility in real time, approving or declining the BNPL option.

-

Repayment Timeline: The total sum is divided equally across installments, with each payment automatically deducted on specified dates.

-

Fees & Interest: In general, no extra fees apply as long as payments are made on time. However, users who miss or delay payments may incur penalties, depending on local regulations.

Advantages and Challenges

-

Advantages:

-

Seamless integration with PayPal’s already-popular checkout.

-

Availability in multiple countries with varying installment structures.

-

Zero or minimal interest for short-term installments.

-

-

Challenges:

-

Global Policy Variations: Different rules per region can create confusion for international shoppers or frequent travelers.

-

Competition from Banks and Other BNPL Providers: PayPal must constantly innovate to keep pace with a market full of traditional banks, startups, and alternative fintech solutions.

-

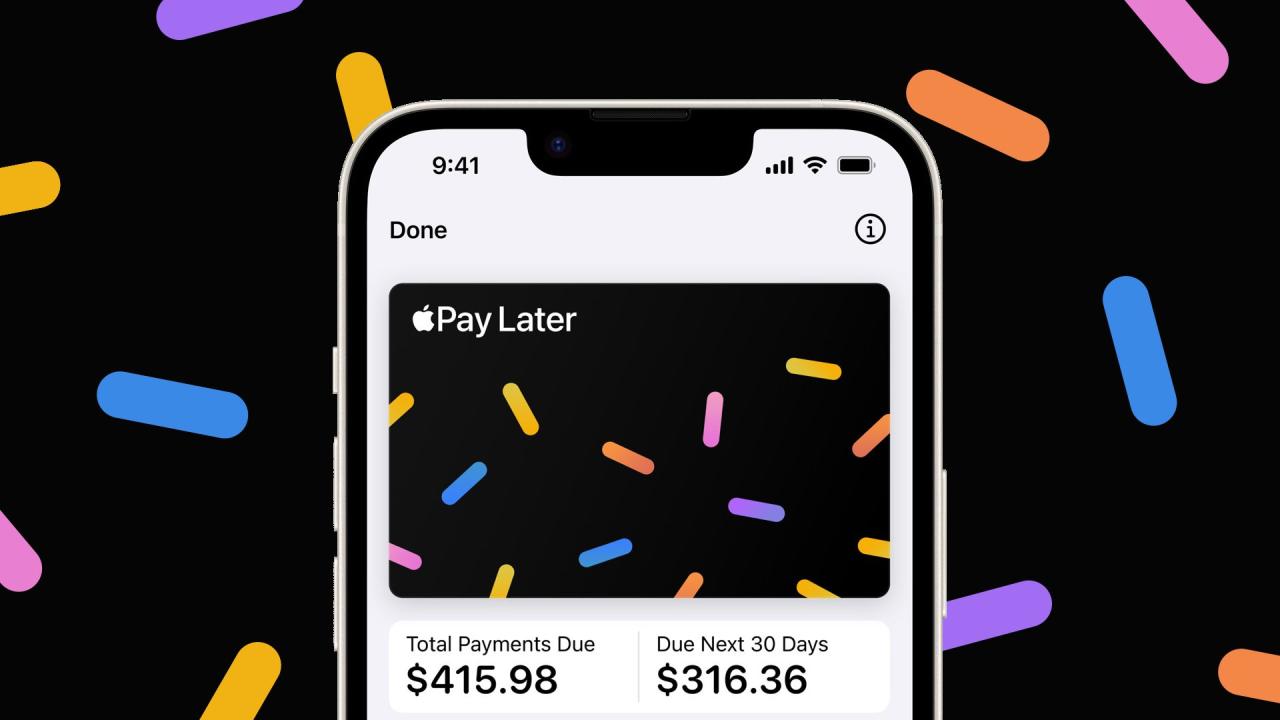

3. Apple Pay Later: Ambitions and Limitations

Launch and Compatibility

-

Recent Release: Apple Pay Later debuted in October 2023, exclusively in the United States.

-

Ecosystem Centered: As part of Apple Pay, the service was seamlessly integrated into iOS devices, ensuring a consistent user experience—similar to Apple Card or Apple Cash.

-

Merchant Acceptance: Apple Pay Later only worked where Apple Pay is accepted; many physical and online merchants in the U.S. support Apple Pay, making initial adoption smoother for Apple users.

How It Worked

-

Four Installments, Six-Week Window: Users could divide their purchase into up to four payments, with the first payment acting like a down payment.

-

Zero Additional Fees: Apple promised no administrative fees or hidden costs. As long as each installment was paid on time, the user wouldn’t encounter interest or late fees.

-

Payment Extension Feature: Users had the option to postpone due dates for certain installments directly in the Wallet app, providing an extra layer of flexibility not typically seen in other BNPL services.

Why Apple Pay Later Was Poised for Impact

-

Apple Ecosystem Synergy: The more integrated Apple Pay became (across the iPhone, iPad, Apple Watch, Mac, and associated apps), the higher the likelihood consumers would opt for Apple’s proprietary BNPL solution rather than turn to a third-party option.

-

Security and User Trust: Apple’s brand reputation for privacy and security gave prospective users increased confidence, especially when compared to older platforms with checkered security records.

-

User Growth Projections: Analysts anticipated Apple Pay’s user base to exceed 56.7 million by 2026, fortifying the BNPL’s potential user reach.

4. Comparing PayPal Pay Later and Apple Pay Later

Despite their similarities, PayPal Pay Later and Apple Pay Later differentiated themselves in core ways:

-

Platform Ecosystem

-

PayPal: Multi-platform approach with broad acceptance across countless e-commerce sites globally. Users can shop on various platforms using web browsers or mobile apps.

-

Apple: Firmly rooted in Apple’s hardware and software environment, offering a unified experience for iPhone, iPad, Mac, and Apple Watch owners.

-

-

Geographical Reach

-

PayPal: Available in many countries with different BNPL policies.

-

Apple: Limited to the U.S. for the Apple Pay Later launch. The global expansion potential was uncertain from the outset.

-

-

Installment Structure

-

PayPal: Generally, four payments across six weeks in the U.S. with expansions or variations in other markets (e.g., three installments in the UK, four in France and Australia).

-

Apple: Strict four-payment plan over up to six weeks, with down payment required, and an option to extend deadlines on some purchases.

-

-

Fees and Interest

-

PayPal: Usually no interest for short-term installment plans, but issues can arise if a payment is late.

-

Apple: Zero fees or interest—intended to replicate the brand’s “it just works” mantra.

-

-

User Experience

-

PayPal: Widespread acceptance but faced criticisms regarding user data management and occasional security concerns.

-

Apple: Maintained a minimalistic, privacy-focused approach—although adoption was limited by Apple’s hardware ecosystem and merchant acceptance of Apple Pay.

-

5. Market Impact and Investor Sentiment

PayPal’s Early Dominance, Then Competitive Struggles

-

Early BNPL Leadership: When PayPal introduced its Pay Later feature in 2021, it quickly became a leading BNPL provider in the U.S. due to PayPal’s ubiquitous checkout presence.

-

Growing Competition: Other startups (Affirm, Klarna, Afterpay) and established tech players (Apple, Google) jumped into the BNPL space, intensifying the fight for customer loyalty.

-

Investor Confidence Fluctuation: Facing pressure from Apple Pay Later and other BNPL apps, PayPal experienced challenges in market share retention. Concerns about data security and outdated user experiences contributed to a slump in investor confidence, forcing PayPal to focus on refining user experience and bolstering security measures.

Apple Pay’s Momentum and Ecosystem Advantages

-

Continuous User Growth: Analysts projected Apple Pay’s user base to keep expanding well into 2026. Apple’s track record in brand loyalty suggested many existing iPhone users would incorporate Apple Pay into daily shopping routines.

-

Stronger Integration: Apple’s deep hardware-software integration typically leads to a smoother user experience, making Apple Pay appealing as a frictionless, secure payment method.

-

Pressure on Legacy Providers: Apple’s entry placed immediate pressure on older digital payment providers, including PayPal, Visa, and Mastercard, who had to innovate faster to compete.

Shifts in Q1 2024: PayPal’s Positive Performance

-

Revenue Uptick: In Q1 2024, PayPal reported improved revenues and higher transaction volumes. This slight rebound hinted that PayPal’s strategy of improved UX and more robust security might be paying off.

-

Investor Reactions: Despite Apple’s brand advantage, PayPal’s ability to reclaim some lost ground revived partial investor optimism—indicating the BNPL competition wouldn’t be a one-sided race after all.

6. The Surprise Decision: Apple Pay Later Discontinued

In a twist, Apple’s board of directors decided to discontinue Apple Pay Later—a move few industry observers anticipated. According to Apple’s statements, the company aims to prioritize new types of financing options, including:

-

Installment Plans from Eligible Debit or Credit Cards: Instead of Apple carrying BNPL loans, Apple may allow card issuers to handle installments within the Apple Wallet, offering a broader array of interest rates and credit checks.

-

Third-Party Integrations (e.g., Affirm): Apple could pave the way for Affirm or other BNPL specialists to integrate deeper into Apple Pay, freeing Apple from managing its own BNPL underwriting.

-

Expanding Apple Card’s Capabilities: The existing Apple Card might be enhanced to offer flexible payment plans, effectively covering BNPL without the separate Apple Pay Later branding.

Why Might Apple Retreat?

-

Risk and Regulatory Landscape: BNPL services face growing scrutiny by regulators worried about consumer debt, requiring compliance overhead Apple may prefer to avoid.

-

Profit vs. Brand Reputation: In-house BNPL might yield modest profit margins but expose Apple to credit risks. Apple’s brand thrives on an easy, secure user experience—managing credit risk doesn’t align with Apple’s core competencies.

-

Focus on Ecosystem Partnerships: Apple historically collaborates with financial institutions (Goldman Sachs for Apple Card, for instance) to handle the complexities of credit and underwriting.

7. Looking Ahead: Implications for Users, Merchants, and Investors

-

Users

-

With Apple Pay Later discontinued, Apple-centric shoppers will shift back to other BNPL providers or rely on standard credit card installments.

-

Users might see more robust BNPL solutions from Affirm or card issuers integrated into Apple Pay, possibly offering competitive rates and specialized deals.

-

-

Merchants

-

Initially, merchants that had begun accommodating Apple Pay Later will adapt, likely reinstating other BNPL options like PayPal Pay Later or Affirm, which remain widely recognized.

-

Apple Pay’s continued expansion ensures the contactless payment remains a strong method. The disappearance of Apple Pay Later doesn’t diminish Apple Pay’s convenience.

-

-

Investors

-

Some investors who viewed Apple’s BNPL entry as a step toward a diversified fintech strategy might temper their expectations. Apple remains strong, though, and can still leverage other financial offerings (Apple Card, Apple Cash).

-

PayPal potentially benefits, facing less immediate BNPL pressure from Apple. Still, it must continue refining user experience and security to combat other emerging contenders.

-

-

BNPL Sector

-

The BNPL sector remains highly competitive with Affirm, Klarna, Afterpay, and PayPal leading the charge. Apple’s short-lived foray underscores the complexities and regulatory hurdles of in-house BNPL solutions.

-

This incident may pave the way for deeper collaborations between Apple Pay and specialized BNPL players, offering flexible financing without Apple shouldering credit liabilities.

-

Conclusion

The rise and sudden discontinuation of Apple Pay Later highlight just how dynamic the BNPL market can be. Both Apple Pay Later and PayPal Pay Later aimed to enhance convenience, provide user-friendly payment installments, and cultivate loyalty within their respective ecosystems. Yet their divergent outcomes reflect the difficulties of managing BNPL services amid evolving consumer demand, regulatory oversight, and brand strategy.

-

PayPal’s Continued Role: Despite encountering stiff competition, PayPal’s well-established brand, large user base, and recent improvements suggest PayPal Pay Later will remain a preferred BNPL method for many consumers, especially as it expands or adapts globally.

-

Apple’s Fintech Future: Even though Apple Pay Later has ended, Apple’s overall payment and finance strategy remains robust. The company’s emphasis will likely shift to forging partnerships with leading banks, credit card issuers, or BNPL players to streamline the Apple Wallet experience—thus staying relevant without incurring the risks of direct BNPL management.

Ultimately, for consumers, the BNPL marketplace still brims with options. While Apple Pay Later’s discontinuation might be disappointing for some, users can still utilize PayPal Pay Later or other established BNPL providers. And for Apple fans, it’s reasonable to expect new and refined in-wallet financing solutions—an evolution that aligns with Apple’s brand philosophy of prioritizing secure, frictionless user experiences above all else.

{kind=link}